Going Digital in the Incumbent Insurance World

The insurance world is broad, with complex products ranging from life insurance and liability insurance for large corporates, to on-demand car insurance and AI-powered watch insurance.

The changes in how people work—notably the rise of the gig economy—has opened up entirely new markets for both incumbents and startups alike.

While most of us within the digital financial services world are well up to speed on how incumbent banks are going digital, the insurance industry has quietly been following suit, albeit at a slower pace. Incumbent insurers are following the same routes as traditional banks in how they launch fully digital propositions including:

Creating entirely digital spin-offs

Partnering with Insurtech-as-a-Service providers to quickly launch new, often niche solutions

In this article we will explore how long standing insurers are beginning to fully digitise their offering via these routes.

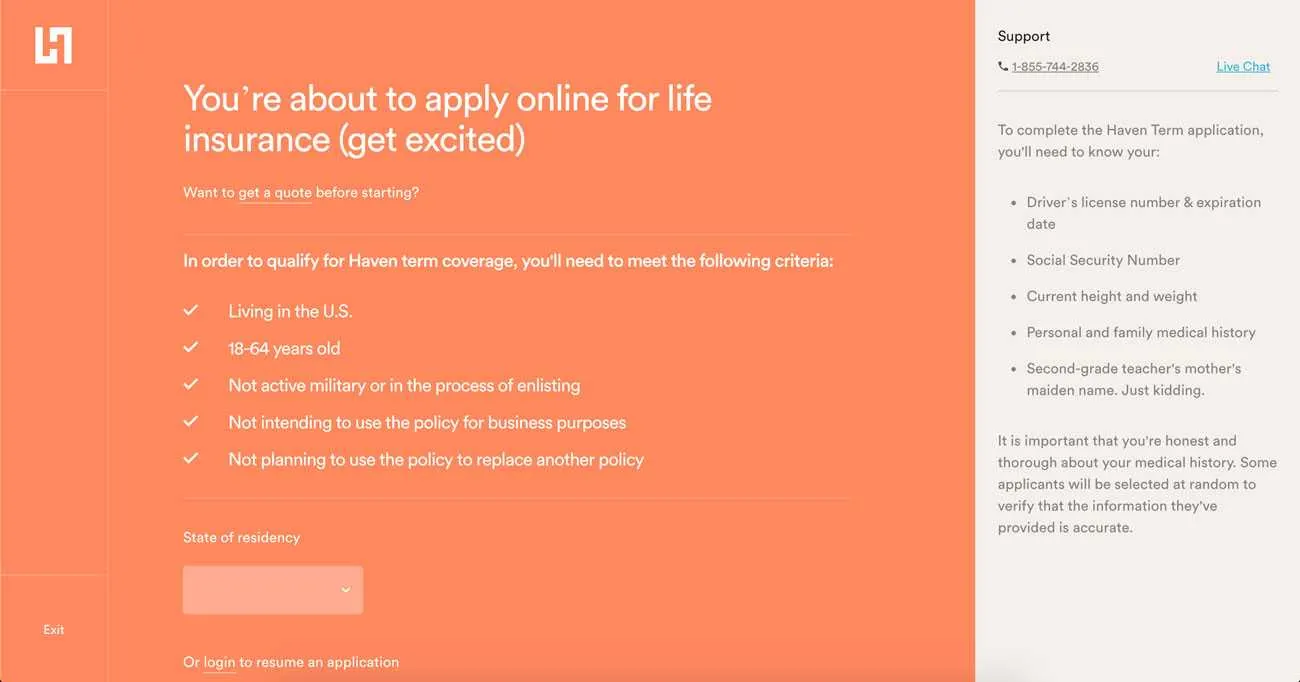

Reimagining life insurance: the spin-off

Haven Life is a completely digital offshoot of MassMutual that exclusively sells life insurance policies. Haven Life aims to tackle the arduous process of taking on a life insurance policy by offering (successful) customers life insurance in 20 minutes, entirely online. The life insurance market in the US has some inherent pain points:

Heavy regulation

The need for a physical medical exam, prohibiting instant fulfilment

Long arduous applications, that were often on- and offline (although primarily offline).

Haven Life looked to become a 'proper Insurtech' from Day 1, by aiming to be mobile-first, customer-focused, simple and fully digital. From the earliest stages of development— to create a fully customer-centric approach—Haven Life needed to create a product that was as real-time as possible and entirely digital.

From the start, the largest challenges presenting a fully-digital life insurance product were the amount of questions customers were required to answer, as life insurance is an incredibly data heavy product, and the lack of real-time decisioning prohibited by the need for a physical medical exam.

Haven Life tackled these two pain-points by taking the typical burden of extensive questions and extensive waiting times away from the customer. The secret sauce to achieving this is utilising smart data, and tapping into the data of its parent, MassMutual. Haven Life offers instant fulfilment by bringing in real-time data and running it through algorithms, and uses the mortality data and expertise of MassMutual to reduce the time and number of questions, building a new approach to underwriting. In addition to utilising data from MassMutural, it also confirms data with third party vendors like the Medical Information Bureau, the DMV and the Social Security Administration.

Haven Life also incorporates other digital components, such as e-signatures, online payments and digital payment reminders.

This idea of “taking the burden away from the customer and back onto us” is something that isn’t necessarily natural for incumbent institutions to implement, both from the technical perspective, and from the product owner mindset.

Historically incumbents have been able to create customer experiences based on what suits their business and operating model. However, with the rise of insurtechs, they are forced to re-think the customer experience, which is often driven by technology and deep customer insights research.

Haven Life has shown that the more that burden can be taken on by the insurer, the more they can win over customers. They have an NPS score of 74 right now, 30 points above industry average

Haven can then focus on ensuring the experience is fully digital, and not just partly digitised. One of the benefits of taking the “digital off-shoot” route is that the entire customer experience, technology, and method of product build can be entirely in your hands.

Rapid product development: Insurtech-as-a-Service

While completely digital off-shoots continue to launch, incumbents can utilise Insurtech-as-a-Service providers to rapidly launch new digital products and services.

Key players in this space include Hitachi Consulting, whose clients include SVD and Aegon Life; Genasys Technologies, whose clients include Standard Bank, Old Mutual, Aon, and Kasko.

The latter is a well established player, partnering with leading insurers in Europe, notably the DACH (Germany, Austria, Switzerland) region. Kasko helps insurers act like insurtech startups by allowing companies to design, distribute and run digital insurance products.

Kasko supports companies and incumbents on the front-end and customer facing part in addition to the technology side. It offers flexible product designs with integrated customer journey builders including application and policy management via REST APIs or white-labeled web apps. By using Kasko, functional products can be delivered in as little as 6 weeks, and the average cost for front-end development is EUR 30,000 - EUR 50,000.

As mentioned, Kasko has a great track record working with incumbents, such as AXA, Allianz and Baloise. It also works with incumbents in other verticals that are interested in augmenting their existing offering with an insurance product. This is particularly prevalent in the automobile and travel sectors. Some of the new products Kasko has helped launch include:

On-demand insurance, specifically for test drives in private automobile sales. This is in partnership with AutoScout 24, one of Europe’s largest internet car marketplaces.

The first cyber-insurance product in Switzerland, developed for Baloise in their direct channels and then subsequently offered by Swiss banks. The insurance covers consumers against cyber world risks such as ensuring photos posted online that the customer is not happy with are deleted, or any costs incurred for fraudulent card use.

Watch insurance, powered by AI available for Swiss customers via Baloise

Pay per kilometer insurance, offered by FRIDAY in collaboration with Kasko.

Similar to what we see in the traditional banking world, where incumbents partner with established BaaS providers to launch new services, the clear benefit here is using the latest tech, typically API-led, that can be siloed from existing legacy systems.

Another benefit is access to pre-built front-end solutions, minimising the time to launch. All of these benefits manifest themselves in the increasing partnerships between incumbent insurers and Insurtech-as-a-Service providers.

Considerations to make when looking to begin your digital journey

Whether you are an incumbent insurer, or a large player in a non-financial market looking to expand your value proposition by offering an insurance product, there are plenty of opportunities to launch a customer-centric, digital solution. There are a handful of considerations before you decide which route is best including:

Distribution channels: will you sell direct via your app or website, will you offer your product via a marketplace (e.g. Starling)?

Underwriting: will you use an established underwriter or, if you have the underwriting capabilities, will you leverage these?

Data: how will you capitalise on smart data to take the burden away from the customer? Who can you partner with to provide a customer experience that is instant, personalised and relevant?

The insurance sector, similar to traditional banking, has experienced a wave of new, customer-centric digital products and services. In the banking space, this has been largely driven by fintechs, and now the insurance sector is seeing its own wave of Insurtech disruption.

Furthermore, this is taking place across the entire insurance industry, from life to travel insurance verticals. In the next article we will explore further how these new solutions have solved real customer pain points.

Photography — Ricardo Resende for Unsplash